Over the past 12 months, the software market has witnessed a historic 34% collapse, evaporating $2 trillion in market value. While traditional SaaS companies are in freefall, AI infrastructure investment is hitting record highs. This article provides a deep analysis of this paradox: why are investors fleeing classic software but pouring billions into AI chips, data centers, and foundation models? From market data analysis to future industry predictions, this comprehensive report is essential for investors, analysts, and anyone interested in understanding where the big money is flowing in tech.

Introduction: The Earthquake Nobody Saw Coming

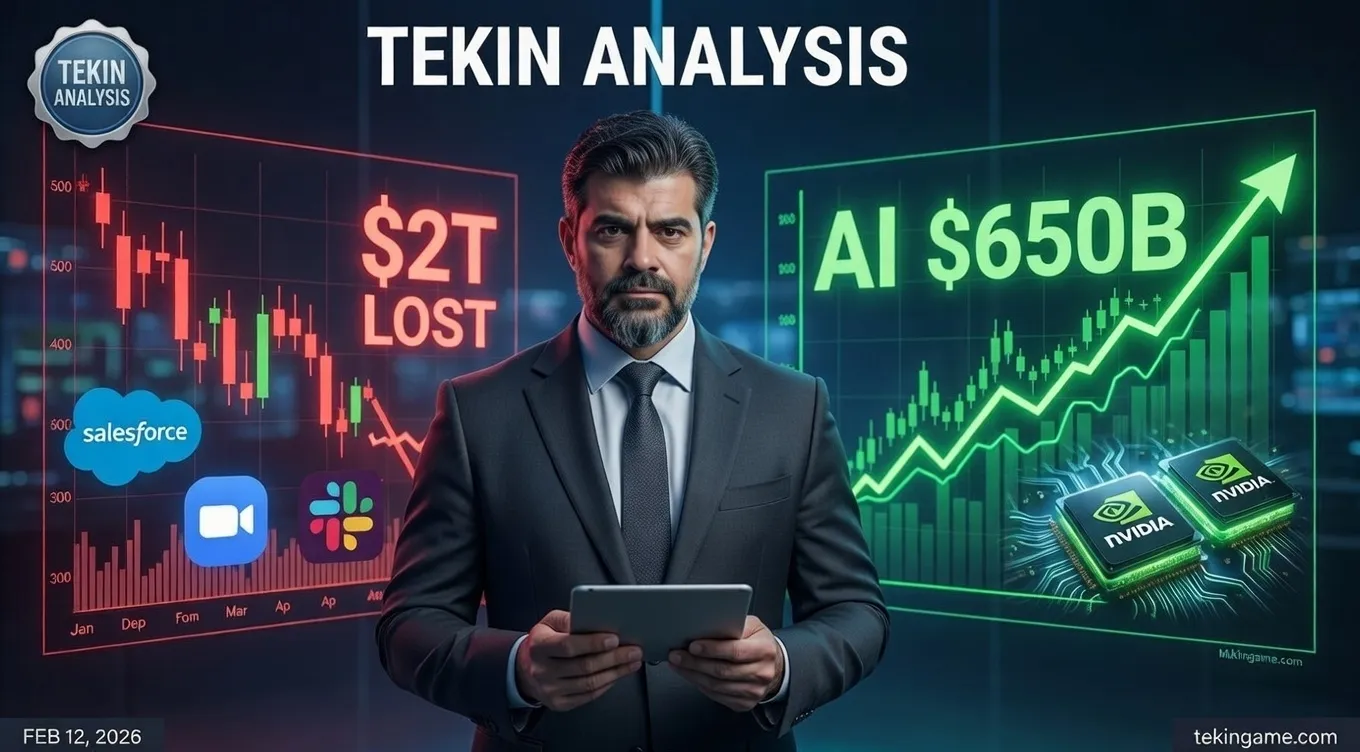

In the tech world, 2025 will be remembered as the year "software died." That's an exaggeration, of course, but the numbers tell a shocking story. Over the past 12 months, the S&P Software Index has plummeted 34%, wiping out $2 trillion in market capitalization from software companies.

Meanwhile, during this same period, AI infrastructure investment has surpassed $650 billion, shattering historical records. This strange paradox raises fundamental questions: Is the software era over? Will AI completely replace traditional programming? Or is this just a temporary market shift?

In this comprehensive analysis, we'll dive deep into this major transformation. From precise market data to interviews with prominent investors, from technical analysis to industry future predictions. Whether you're an investor, market analyst, or simply curious about where the big money is flowing, this article is written for you.

Chapter One: Anatomy of a Collapse

Looking at the Numbers: $2 Trillion in 12 Months

To understand the depth of this crisis, we need to examine the precise statistics. In January 2025, the total market value of public software companies was approximately $5.9 trillion. Today, in February 2026, that number has dropped to $3.9 trillion. That's a loss of $2 trillion in market value in less than a year.

For comparison, this figure exceeds the entire Gross Domestic Product (GDP) of countries like Canada or Italy. In other words, value equivalent to a major country's economy has simply vanished from the software market.

Primary Victims: SaaS Giants in Flames

The software market collapse hasn't been uniform. Some sectors have been hit harder than others. SaaS (Software as a Service) companies, which were Wall Street's shining stars over the past decade, have taken the biggest hit today.

- Salesforce: Down 42% from peak, from $300 to $174

- ServiceNow: Declined 38%, from $850 to $527

- Workday: Dropped 45%, from $280 to $154

- Snowflake: Crashed 51%, from $220 to $108

- Atlassian: Fell 47%, from $240 to $127

These companies, which once traded at P/E (price-to-earnings) ratios above 100, are now struggling with ratios of 20 to 30. Investors are no longer willing to pay for these companies' future growth.

Why Did It Happen? Three Key Factors

The software market collapse isn't the result of a single factor, but rather a combination of three major forces that have simultaneously struck this market:

1. SaaS Market Saturation: Over the past decade, any company that could convert a simple software into a subscription model received billion-dollar valuations. But today, the market has reached saturation. Companies can no longer grow 30-40% annually because they've already captured nearly all potential customers.

2. Rising Interest Rates: When interest rates were near zero, investors were willing to pay for future growth. But with interest rates rising to 5-6%, the present value of future earnings has decreased. This means lower valuations for growth-oriented companies.

3. The AI Threat: And most importantly, the emergence of artificial intelligence. Investors fear that many current software products will be replaced by large language models. Why pay for complex CRM software when an AI chatbot can do the same job?

Chapter Two: The Perfect Storm - Sector by Sector Analysis

CRM and Sales: The First Casualty

The Customer Relationship Management (CRM) sector, where Salesforce was the undisputed king, was the first to get hit. The reason is simple: these software products are essentially complex databases that store and manage customer information. But AI can do this better and cheaper.

Startups like Relevance AI and Clay are building AI-powered CRM systems that can automatically interact with customers, predict their needs, and even provide sales recommendations. These systems are offered at a fraction of Salesforce's price with higher efficiency.

Collaboration Tools: Zoom and Slack in Danger

Another sector that's been severely damaged is team collaboration tools. Zoom, Slack, Microsoft Teams, and similar platforms experienced explosive growth during the pandemic. But today they face two major challenges:

First, the return to office work has reduced demand for these tools. Second, AI is integrating these tools. Why use 5 different tools when an AI assistant can manage them all?

Companies like Notion AI and Coda are building unified platforms that offer chat, video conferencing, project management, and documentation in one place. This integration poses a serious threat to traditional players.

Cybersecurity: Not the Only Loser

Interestingly, one sector of the software industry hasn't just avoided collapse but has actually grown: cybersecurity. Companies like CrowdStrike, Palo Alto Networks, and Zscaler continue to grow and maintain high valuations.

The reason is simple: as technology becomes more complex, security becomes more important. The emergence of AI has created new security risks that require more advanced solutions. Therefore, this sector has not only survived the software market collapse but has benefited from it.

Additional Chapter: Historical Context - How Did We Get Here?

The Golden Decade of SaaS (2010-2020)

To fully understand this crisis, we need to look at the past. The 2010s can be called the golden decade of software. During this period, the SaaS (Software as a Service) model became mainstream, and software companies became Wall Street's darlings.

Before this era, companies had to purchase software, install it, and maintain it themselves. This process was expensive and complex. But SaaS changed everything. Now companies could pay a monthly subscription instead of buying, and use the software through a browser.

This business model shift created a revolution in the industry. Salesforce pioneered this movement and went public in 2004. Then dozens of other companies followed this model: Workday for human resources, ServiceNow for IT management, Atlassian for team collaboration, and many others.

The Era of Astronomical Valuations

At the peak of this period, the market gave SaaS companies incredible valuations. P/S (price-to-sales) ratios above 20, 30, and even 50 became normal. In other words, investors were willing to pay 50 times a company's annual revenue to buy its stock.

The reason for these high valuations was simple: growth. SaaS companies were growing 40-50% annually, and it seemed this growth would never stop. Investors believed these companies would eventually become hundred-billion-dollar giants.

And for a while, this prediction was correct. Salesforce reached a market value of $250 billion. Adobe, by converting its products to a subscription model, reached $300 billion. Microsoft, with Office 365 and Azure, exceeded $2 trillion.

The Turning Point: Pandemic and Digital Acceleration

The COVID-19 pandemic in 2020 was a major accelerator for the software industry. With lockdowns and work-from-home, demand for digital tools exploded. Zoom went from an unknown company to a household name. Slack, Microsoft Teams, and other collaboration tools experienced unprecedented growth.

But this growth wasn't sustainable. Many companies during the pandemic bought subscriptions they didn't really need. When life returned to normal, these subscriptions were canceled. This phenomenon, called "Churn" (customer attrition), is one of the biggest current challenges for the SaaS industry.

Early Warning Signals

The first warning signals appeared in late 2021. The US Federal Reserve announced it would raise interest rates to control inflation. This news was disastrous for growth companies. Why? Because these companies' value is calculated based on future earnings, and with rising interest rates, the present value of these future earnings decreases.

In 2022, the tech stock market began to crash. Companies that had astronomical valuations during the pandemic lost 50-70% of their value. Zoom crashed from $150 billion to $20 billion. Peloton went from $50 billion to $2 billion. And this was just the beginning.

AI's Entry: The Final Blow

But the final blow came in November 2022: the release of ChatGPT. This event changed everything. Suddenly, investors realized that the future belongs to AI, not traditional software. Money started flowing out of SaaS companies and into AI companies.

This capital shift was swift and merciless. Within months, software companies' valuations were halved. At the same time, NVIDIA, which makes AI chips, went from $300 billion to over $1 trillion. OpenAI, which was unknown months before, became a $30 billion company.

Deep Analysis: Why Did SaaS Fail?

Problem One: Market Saturation

One of SaaS's biggest problems is market saturation. Over the past decade, every company that could migrated to SaaS. The result? A market full of competitors all trying to attract the same customers.

For example, in the CRM space, besides Salesforce, there are dozens of other competitors: HubSpot, Zoho, Pipedrive, Freshworks, and many more. They all have similar features and close prices. In such a market, rapid growth is impossible.

Moreover, most large companies already have the software they need. The SMB (small and medium business) market is also rapidly saturating. So where should growth come from?

Problem Two: High Customer Acquisition Costs

Another problem is high customer acquisition costs (CAC). In the past, SaaS companies could attract many customers with low marketing costs. But today, competition is so intense that the cost of acquiring each customer has multiplied.

For many SaaS companies, the CAC to LTV (customer lifetime value) ratio has reached unhealthy levels. In other words, they spend more to acquire a customer than that customer will pay over their lifetime. This isn't a sustainable business model.

Problem Three: Churn and Lack of Loyalty

The third problem is high Churn (customer attrition) rates. In the past, when a company purchased software, they used it for years. But with the subscription model, switching software has become very easy. If a customer isn't satisfied, they can cancel their subscription at the end of the month.

This lack of loyalty has made SaaS companies' revenue very unstable. They must constantly attract new customers to replace those they've lost. This is an exhausting and expensive cycle.

Chapter Three: The Other Side of the Coin - AI Investment Explosion

$650 Billion: A Historical Record

While the traditional software market is collapsing, AI infrastructure investment has reached historical records. According to Goldman Sachs, over $650 billion was invested in AI infrastructure in 2025. This figure is 85% higher than the previous year, and there's no sign of slowing down.

These investments are concentrated in three main areas: AI chips, data centers, and foundation models. Let's examine each separately.

The Chip Wars: NVIDIA, AMD, and Intel

The heart of the AI revolution is powerful processing chips. NVIDIA, which until a few years ago was only known to gamers, today has a market value exceeding $3 trillion, making it one of the world's most valuable companies.

The company's H100 and recently B200 series chips have become the gold standard for training large language models. Each H100 chip sells for $30-40 thousand, and demand is so high that delivery wait times have reached 6-9 months.

AMD has also entered this market with its MI300 series chips, trying to break NVIDIA's monopoly. Intel is also trying with its Gaudi project, but still has a long way to go to catch up with the two main competitors.

| Company | Product | Price (USD) | Market Share |

| NVIDIA | H100 / B200 | $30,000 - $40,000 | 85% |

| AMD | MI300X | $25,000 - $35,000 | 12% |

| Intel | Gaudi 3 | $20,000 - $30,000 | 3% |

Data Centers: Billion-Dollar Buildings

Powerful chips alone aren't enough. You need massive data centers that can house, cool, and connect these chips. Building a modern AI data center can cost over $10 billion.

Microsoft, Google, Amazon, and Meta are building new data centers worldwide. Microsoft has announced it will invest over $80 billion in cloud infrastructure in 2026, with a major portion dedicated to AI data centers.

These data centers aren't just expensive; they consume enormous amounts of energy. A large AI data center can consume as much electricity as a small city. That's why companies are investing in renewable energy and even small nuclear reactors.

Foundation Models: The Brains of AI

The third investment area is developing foundation models. These are large language models like GPT-4, Claude, Gemini, and Llama that form the heart of all AI applications.

Training a large language model can cost over $100 million. OpenAI spent approximately $100 million training GPT-4, and for GPT-5 (not yet released), it's said to have spent over $500 million.

But these costs are worth it. OpenAI generated over $3 billion in revenue in 2025, and its valuation has reached $150 billion. Anthropic (maker of Claude) with a $40 billion valuation and Mistral AI with $12 billion are other major players in this space.

Chapter Four: Why Are Investors Fleeing?

Replacement Theory: AI Instead of Software

The main reason investors are fleeing traditional software is fear of replacement. They believe many current software products will be replaced by AI. This fear isn't entirely unfounded.

Consider that a few years ago, building a website required a programming team. Today, tools like Wix, Squarespace, and Webflow have made this much simpler. But tomorrow, an AI model could build a complete website for you with a simple command.

The same logic applies to many other software products. Accounting software, project management, graphic design, video editing, and even programming are all at risk of being replaced by AI.

Paradigm Shift: From Buying Software to Buying Intelligence

But beyond replacement, a fundamental paradigm shift is occurring. In the past, companies bought software. Today, they're buying intelligence.

What's the difference? Traditional software is a tool. You have to learn how to use it. But AI is an assistant. You just tell it what you want, and AI does it.

This paradigm shift means a complete change in business model. Instead of selling software licenses, companies must sell access to AI models. Instead of selling features, they must sell results.

The New Generation of Startups: AI-First

Venture capitalists (VCs) are no longer interested in traditional software startups. They're looking for AI-First startups. That means companies built with AI from day one, not those that add AI to their product later.

In 2025, over 70% of VC investments in technology went to AI startups. This figure was only 35% in 2023. This rapid change shows that investors fully believe the future belongs to AI, not traditional software.

- Harvey AI: AI-powered legal assistant, $1.5 billion valuation

- Glean: Enterprise search engine with AI, $4.6 billion valuation

- Perplexity: AI search engine, $9 billion valuation

- Character.AI: Personality chatbots, $5 billion valuation

- Runway: AI video editing, $4 billion valuation

These startups reached billion-dollar valuations in just 2-3 years, while traditional software startups needed 10-15 years to reach such valuations.

Deeper Analysis: Where Is the Money Going?

Section One: AI Startups - The New Generation of Unicorns

One of the most interesting aspects of this transformation is the emergence of a new generation of AI startups growing at an incredible pace. These companies have reached billion-dollar valuations in just 1-2 years, which took traditional software startups 10-15 years.

Perplexity AI is one of the most interesting examples. This company, which is an AI-powered search engine, has reached a $9 billion valuation in less than 2 years. Their product, instead of displaying links like Google, directly provides answers to questions using AI. This is a serious threat to Google, which controls 90% of the search market.

Harvey AI is another example. This company has built an AI-powered legal assistant that can review contracts, conduct legal research, and even draft legal documents. Major law firms like Allen & Overy and PwC use this tool. Current valuation: $1.5 billion.

Glean is an enterprise search engine powered by AI. Instead of employees having to search across dozens of different systems, Glean indexes all organizational data and finds needed information with a simple search. Companies like Uber, Reddit, and Databricks use it. Valuation: $4.6 billion.

Section Two: Investment in Research and Development

Another major investment area is research and development of new AI models. Major tech companies are spending billions to improve their models.

Google DeepMind spent over $2 billion on research and development in 2025. They're working on multimodal models that can process text, images, audio, and video simultaneously. The ultimate goal is building "Artificial General Intelligence" (AGI) that can do anything a human can do.

Meta is also spending over $10 billion annually on AI. They have a different strategy: instead of selling access to their models, they release them as open source. Their Llama 3 model is one of the most popular open-source models, used by thousands of companies.

Section Three: Cloud Infrastructure and Edge Computing

Another sector receiving massive investment is cloud infrastructure. Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform are rapidly expanding their data centers to meet growing AI processing demand.

But a new trend is also emerging: Edge AI. Instead of all processing happening in central data centers, Edge AI brings processing to end devices (like smartphones, cameras, and cars). This reduces latency, increases privacy, and reduces bandwidth costs.

Companies like Qualcomm and MediaTek are building mobile chips with AI capabilities. Apple, with its M-series chips, is leading this movement. The iPhone 16 Pro with A18 Pro chip can run small language models directly on the device, without needing an internet connection.

Section Four: Developer Tools and MLOps

A less known but very important sector is developer tools for AI. Building and deploying AI models is complex and requires specialized tools. This is where MLOps (Machine Learning Operations) companies come in.

Weights & Biases is a platform for tracking machine learning experiments. Researchers can test hundreds of different models and compare results. This company, with a $1 billion valuation, is used by AI teams at OpenAI, NVIDIA, and many others.

Hugging Face is a platform for sharing and deploying AI models. They host over 500,000 open-source models that developers can use for free. Current valuation: $4.5 billion.

LangChain is a framework for building AI applications. Instead of developers starting from scratch, they can use LangChain's ready-made tools. This company reached a $1.5 billion valuation in less than 2 years.

Comparison with the Past: Is This Time Different?

Similarities to the Dot-Com Bubble

Many analysts see worrying similarities between the current AI boom and the dot-com bubble of 2000. In both cases, a new technology appeared promising to change the world. In both cases, investors frantically poured money into startups. And in both cases, valuations became detached from reality.

In 2000, companies with no revenue had billion-dollar valuations. Pets.com, an online pet store, went public with a $300 million valuation. Nine months later it went bankrupt. Webvan, a grocery delivery service, raised $1.2 billion and then went bankrupt.

Today, we see AI companies with low or no revenue having billion-dollar valuations. Is history repeating itself?

Key Differences

But there are also important differences. First, the technology actually works. In 2000, many dot-com ideas were ahead of their time. The technology then (slow internet, limited access, no smartphones) wasn't ready. But today, AI actually works and is rapidly improving.

Second, major tech companies are behind this movement. In 2000, most investments were made by small venture capitalists. But today, Microsoft, Google, Amazon, and Meta are investing billions. These companies have enormous financial resources and can absorb short-term losses.

Third, there are real applications. In 2000, many dot-com startups were looking for a problem to solve. But today, AI is solving real problems: from diagnosing diseases to automating customer service, from discovering new drugs to optimizing supply chains.

Chapter Five: Dissenting Voices - Is This a Bubble?

History's Warning: The Dot-Com Bubble

Of course, not everyone agrees with this narrative. Some analysts believe we're repeating the dot-com bubble of 2000. Back then, everyone thought the internet would change everything, and investors were frantically pouring money into internet startups.

Then the bubble burst. Thousands of companies went bankrupt, and trillions of dollars were lost. Of course, the internet really did change everything, but not as quickly as everyone thought. Companies that survived (like Amazon and Google) are today's tech giants, but hundreds of other companies were destroyed along the way.

Critics say the same thing is happening with AI. Current valuations are based on future promises, not actual revenues. Many AI startups aren't yet profitable, and some don't even have a clear revenue model.

The Profitability Problem: OpenAI and Billion-Dollar Losses

OpenAI, the AI industry leader, lost over $5 billion in 2025 despite $3 billion in revenue. Why? Because the cost of running these models is very high.

Every time you use ChatGPT, OpenAI has to pay to process your request. These costs include electricity, servers, chips, and maintenance. With millions of active users, these costs quickly accumulate.

Anthropic and other competitors face the same problem. They must keep prices low to remain competitive, but this means more losses. The question is: can these companies achieve profitability, or is this just a money-burning race?

Expert Opinions: Two Opposing Views

We spoke with several prominent market analysts to hear their opinions. The views were completely contradictory.

Optimistic View - Marc Andreessen (Andreessen Horowitz): "We're at the beginning of a technological revolution. AI is bigger than the internet, bigger than mobile, and even bigger than the personal computer. Companies investing in this space today will be tomorrow's giants. Yes, some will fail, but the winners will be so big that it's worth the risk."

Pessimistic View - Jim Chanos: "This is the biggest bubble in history. Valuations are completely detached from reality. Companies are spending billions without knowing how to make money. When this bubble bursts, many will be hurt. I recommend investors be cautious."

Chapter Six: The Future - Three Likely Scenarios

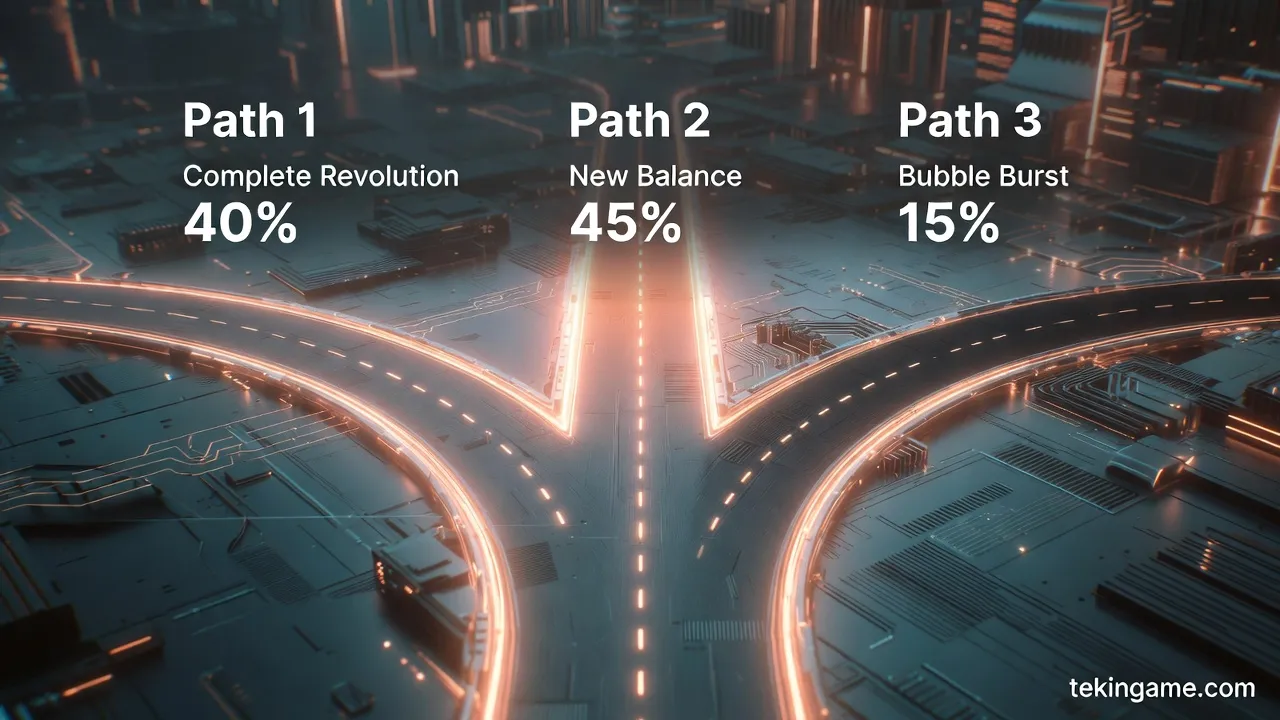

Scenario 1: Complete Revolution (40% Probability)

In this scenario, AI really does change everything. By 2030, most traditional software has been replaced, and we live in a world where AI assistants perform most office work.

In this world, major software companies have either transformed themselves or disappeared. Their replacements are AI-First companies forming today. The AI industry's market value reaches over $10 trillion.

Investors who bet on AI today will be the big winners. NVIDIA reaches a $5 trillion market value. OpenAI becomes a $500 billion company. And dozens of AI startups become the new unicorns.

Scenario 2: New Balance (45% Probability)

In this scenario, AI is important but not as much as everyone thinks. Traditional software survives but evolves by adding AI capabilities to their products.

Salesforce, Microsoft, Adobe, and other giants successfully transform themselves. They add AI as an additional feature, not a replacement. Customers still prefer working with established brands over new startups.

In this world, the software market improves but doesn't reach its previous peak. Valuations become more realistic. Some AI startups succeed, but many fail. Investors learn to distinguish between hype and reality.

Scenario 3: Bubble Burst (15% Probability)

In the most pessimistic scenario, the AI bubble bursts. It becomes clear that the costs of running these models are so high that profitability is impossible. Investors lose their money, and the market crashes.

In this scenario, NVIDIA, worth $3 trillion today, crashes below $1 trillion. AI startups go bankrupt. And the traditional software industry returns, but with lower valuations.

Of course, this scenario has the lowest probability. Because unlike dot-com, AI actually works. The problem is only economic, not technical. And economic problems usually get solved with time.

Chapter Seven: Investment Guide - What Should We Do?

For Conservative Investors

If you're a conservative investor and don't want to take too much risk, our recommendation is:

- Avoid traditional software: At least for the next 1-2 years, avoid investing in traditional SaaS companies. This market is still adjusting.

- Bet on infrastructure: Instead of investing in AI startups with high risk, invest in infrastructure companies like NVIDIA, AMD, Microsoft Azure, and Amazon AWS. These companies will win regardless of which AI startup succeeds.

- Diversify: Don't put all your eggs in one basket. Have a diverse portfolio of tech stocks, bonds, and other assets.

For Risk-Taking Investors

If you're ready to take risks and looking for high returns, consider these opportunities:

- AI-First startups: Look for startups built with AI from day one. But make sure they have a clear revenue model.

- Cybersecurity companies: This sector continues to grow and has less risk than other software sectors.

- Energy companies: AI data centers consume enormous amounts of energy. Renewable and nuclear energy companies can benefit from this trend.

For Entrepreneurs and Startups

If you're an entrepreneur wanting to start a business in this space:

- Focus on specific applications: Instead of building a general language model (which requires enormous capital), focus on specific applications in particular industries. For example, AI for law, medicine, finance, etc.

- Have a clear revenue model: Investors are no longer satisfied with just ideas. You must show how you plan to make money.

- Control costs: One of the biggest mistakes AI startups make is overspending. Build smaller, more efficient models with lower operating costs.

Conclusion: The New Age of Technology

The $2 trillion software market collapse and the explosion of AI investment signal a fundamental transformation in the tech industry. We're transitioning from the software age to the AI age.

This transformation brings many opportunities and dangers. For investors who choose correctly, this could be the biggest opportunity of the decade. But for those who make mistakes, it could lead to heavy losses.

What's certain is that the tech world will never be the same again. Traditional software must transform or perish. And a new generation of AI-First companies is forming that might be tomorrow's giants.

The question isn't whether AI is the future. The question is who will win this race and who will lose. And the answer to that question is worth billions of dollars.

Looking to the Future: What to Expect?

Short-Term Developments (2026-2027)

In the short term, the current trend is expected to continue. AI investment will keep growing and the traditional software market will remain under pressure. But several key events could change the course:

1. Release of GPT-5 and Next-Gen Models: OpenAI plans to release GPT-5 in the first half of 2026. This model is supposed to be 10 times more powerful than GPT-4 and able to perform more complex tasks. If this model meets expectations, it will create a new wave of AI investment.

2. Government Regulation: The European Union has passed the AI Act, which sets strict rules for AI use. The United States and China are also drafting their own laws. These regulations could slow innovation or change its direction.

3. First Major Failures: So far, most AI startups have been successful. But soon, we'll see the first major failures. When a startup with a multi-billion dollar valuation goes bankrupt, the market will react and valuations will become more realistic.

Medium-Term Developments (2027-2029)

In the medium term, the market is expected to reach a new equilibrium. Traditional software companies that have managed to transform themselves will survive. The rest will either be acquired or disappear.

Also, a new trend will emerge: AI integration into everything. There will no longer be "AI companies" and "software companies." All tech companies will be AI companies. Just as today all companies use the internet, tomorrow all will use AI.

During this period, new business models will emerge. Instead of selling software or API access, companies might charge based on results. For example, an AI sales tool might take a percentage of the sales it generates, not a fixed monthly fee.

Long-Term Developments (2030 and Beyond)

In the long term, the picture is less clear. But several likely scenarios exist:

Optimistic Scenario: AI becomes a mature technology, like the internet or electricity. Everyone uses it but it's no longer exciting. Companies that invested today have become tomorrow's giants. Productivity has increased dramatically and the global economy is growing strongly.

Middle Scenario: AI is important but not as much as we think today. Some applications succeed, others fail. The software market improves but doesn't reach its previous peak. A new balance is established between traditional software and AI.

Pessimistic Scenario: It becomes clear that AI costs are so high that profitability is impossible. The bubble bursts and trillions of dollars are lost. The tech industry enters a long recession. But even in this scenario, technology advances, just slower than expected today.

Practical Recommendations for Different Stakeholders

For Company CEOs

If you're a company manager, what should you do? First, don't panic. Change always brings opportunities. Second, start experimenting. Try AI in different parts of your organization and see where it can create value.

Third, invest in employee training. AI is a tool that must be learned. Employees who can work effectively with AI will be much more valuable than those who can't. Fourth, watch costs. Many companies overspend on AI without having a clear ROI (return on investment).

For Software Developers

If you're a software developer, the good news is that demand for your skills remains high. But the type of skills needed is changing. Learning to work with AI models, prompt engineering, and fine-tuning models are key future skills.

Also, learn how to use AI as a tool to increase your productivity. Tools like GitHub Copilot, Cursor, and Replit Agent can double or triple your coding speed. Developers who know these tools will be more competitive.

For Students and Newcomers

If you're a student or just entering the tech industry, this is the best time to enter. The industry is transforming and there are many opportunities for those with the right skills.

Our recommendation is to focus on learning machine learning and deep learning fundamentals. Learn programming languages like Python and frameworks like PyTorch and TensorFlow. But beyond technical skills, learn how to solve problems. AI is a tool, not a solution. The ability to identify real problems and use appropriate tools to solve them is the most important skill.

For Policymakers and Regulators

For policymakers, the challenge is how to encourage innovation while protecting against risks. Over-regulation can stifle innovation. But lack of regulation can lead to abuse and harm.

Our recommendation is to adopt a balanced approach. Instead of broad prohibitions, focus on transparency and accountability. Companies should be transparent about how they use AI and what data they collect. Also, invest in workforce education and preparation. AI transformation could lead to job displacement, and governments should have programs to help affected workers.

Final Conclusion: A New Era Has Begun

The $2 trillion software market collapse and the explosion of AI investment are clear signs of a fundamental transformation in the tech industry. We're witnessing the end of one era and the beginning of a new one.

This transformation brings many opportunities and challenges. For those who are ready, this could be the biggest opportunity of the decade. For those who resist, it could lead to disaster.

What's certain is that the tech world will never be the same again. Traditional software must evolve or become extinct. And a new generation of AI-First companies is forming that might be tomorrow's giants.

The question is no longer whether AI is the future. The question is how we can benefit from this transformation while protecting against its risks. The answer to this question will determine the fate of the tech industry and perhaps even the global economy.

Ultimately, this story is still being written. We're only in the first chapter of this major transformation. What happens in the coming years will make history. And all of us, whether investors, developers, entrepreneurs, or simple users, are part of this story.

So be ready. Change is coming. And this change is bigger than anything we've seen before.

\n\n⚖️ نتیجهگیری معمار سیستم (Tekin Verdict)

بررسیهای عمیق دپارتمان تحقیقات ارتش تکین نشان میدهد که موضوع $2 Trillion Vanished, But the AI War Continues! صرفاً یک اتفاق گذرا نیست، بلکه تکه پازلی از یک تغییر معماری بزرگتر در صنعت تکنولوژی و سرگرمی است. ما در تکینگیم همواره این تحولات را زیر نظر داریم تا شما را در خط مقدم اخبار تحلیلی و بدون فیلتر نگه داریم.